The Magnificent Seven’s Surge and Potential Correction Ahead

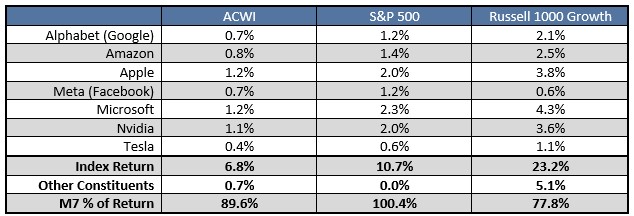

The Magnificent Seven (Apple, Amazon, Alphabet, Microsoft, Nvidia, Meta and Tesla) have significantly outperformed the broader market this year, accounting for nearly 80% of the S&P 500’s return. According to survey data from Bank of America research, the most crowded trade among fund managers today is long mega-cap technology stocks. It is a reasonable assumption that retail participation in these stocks is quite high too.

Table 1: Contribution to Index Return by Magnificent Seven

In 2023, the price-to-earnings valuation of the S&P 500 has hovered between 18-20 times. However, for the Magnificent Seven basket, this ratio has expanded from approximately 23 times at the start of the year to approximately 42 times today. We find this valuation premium excessive, and it is difficult to reconcile how these stock prices have continued to move higher, given the rise in interest rates. To justify this higher ratio, stock prices or interest rates (discount rates) will need to decrease. As of now, the basket has fallen about 11% from its highs in July 2023.

We continue to believe that mega-cap technology stocks may be the most vulnerable to a re-rating (price correction) in a higher for longer environment. As such, our global equity portfolios remain diversified with positions in value, small-cap, and international stocks. In a narrow market like 2023, it takes discipline not to chase what has worked recently, and we would strongly encourage long-term investors to stay the course with their equity exposure.

Fig. 1: High tech valuations leave them vulnerable to re-rating

Magnificent 7 vs. S&P 500 - Multiple Expansion

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2024 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.