Taking the Pulse of US Equities

We’re hearing from an increasing number of investors who recognize the exceptional returns produced by US equities over the last year but wonder if the market has moved too fast.

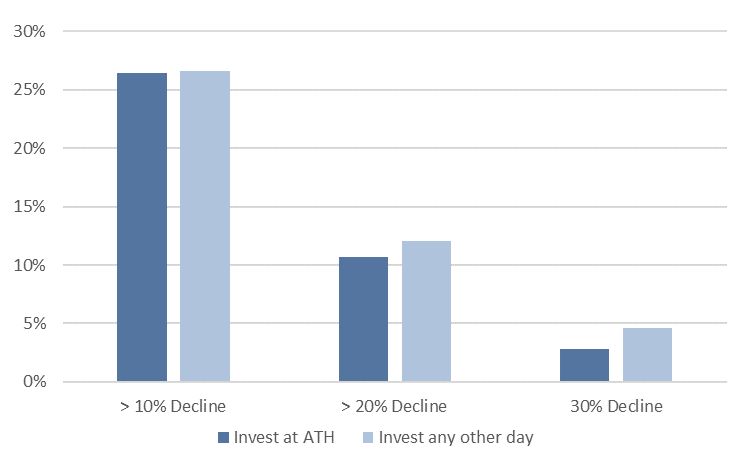

As we published in January, investing at all-time highs has historically resulted in higher returns, not lower returns, than investing on other days. It’s also worth mentioning that historically, we haven’t been more likely to experience a significant drawdown over the next 12 months when we’re at an all-time high (Fig. 1).

The point of mentioning this historical data isn’t that we can’t experience low returns or a significant correction in the near future—it’s that all-time highs are not useful predictors of either of those occurrences.

Fig. 1: Probability of drawdown within 12 months

Here’s how we are thinking about US equities right now (we are overweight US equities in our investment portfolios):

- US equities have performed well due to a combination of factors: (1) optimism about the US economy, (2) optimism about continued earnings growth in the information technology sector, (3) an expectation that earnings growth will resume for non-Mag7 companies, and (4) an expectation that the Fed will ease policy rates in 2024.

- The overall valuation of the US equity market is reasonable at 20x expected 12-month earnings. However, growth equities are trading at 27x expected 12-month earnings versus 16x for value equities.

- The largest companies in the US equity market are also the most expensive from a price-to-earnings perspective. This has led to increased concentration within the US market that subjects the entire market to the fortunes of a few firms. The information technology sector is 30% of the US market, a level not seen since the late 1990s.

- The main risks to the US market, as we see them, are:

-

-

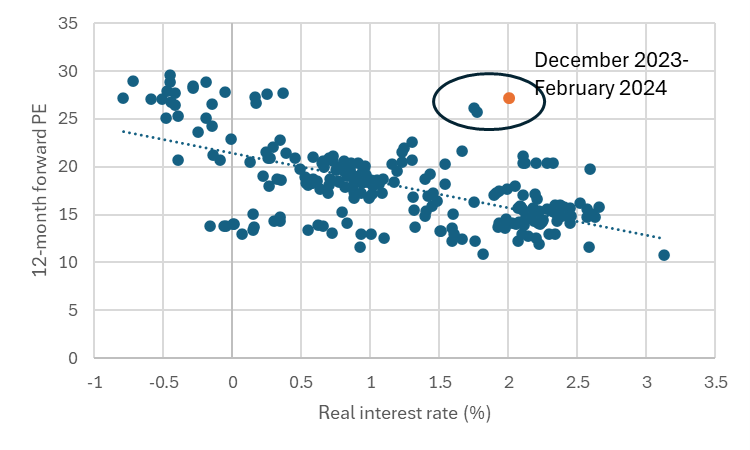

- Hawkish monetary policy: growth equities tend to be more interest rate sensitive than other parts of the market, and current valuations are out of sync with current interest rates (Fig. 2). A repricing higher of expected central bank policy rates could put pressure on mega-cap growth stocks.

- Earnings growth disappointment: consensus earnings growth for information technology is 25% for the next 12 months and 15.5% for the 12 months after that. If earnings disappoint, IT companies would likely see a quick repricing to more reasonable valuations.

- Labor market deterioration: A strong labor market continues to drive economic growth and sustain corporate profits in the US. Cracks in the labor market would be a sign that earnings growth expectations cannot be achieved.

-

Markets always face risks. While we’d prefer a US equity market that was cheaper and not as concentrated, the overall market remains reasonably priced with good momentum. We wouldn’t be surprised to see lower returns and a change of leadership away from the Magnificent Seven (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla) to the other 2993 companies in the US, but there are no immediate signs of cracks in the market or the economic underpinnings of the rally. Maintaining diversification across sectors and geographies is important (You’re Already Heavily Invested in AI) for risk management – particularly at this stage in the cycle.

Fig. 2: US growth equity valuations are out of line with real interest rates

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2024 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.